It’s been called an “appraisal time bomb” by some, while others say it’s no biggie. Today I want to give you the scoop on what it is as well as some of the potential impact it might have.

What is Collateral Underwriter?

Collateral Underwriter (CU) is a property appraisal review tool created by Fannie Mae to help mortgage lenders manage risk.

What will Collateral Underwriter do?

- CU performs an automated risk assessment on appraisals geared toward Fannie Mae and returns a risk score, flags, and messages to the submitting lender. CU will provide a risk score for the appraisal of 1-5 (1 being the lowest risk and 5 being the highest).

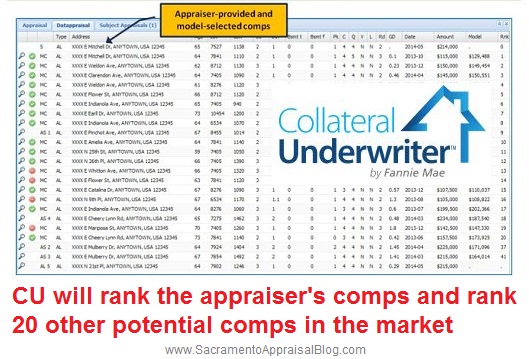

- CU will analyze comparable sales selected by the appraiser and recommend alternatives.

- CU will compare adjustments the appraiser has given with what other appraisers have done in the same area (Fannie Mae has been mining data from over 12 million appraisals since 2011, so they definitely have some data at their disposal).

- CU will use census block groups to analyze market trends.

- CU will review specific information in each appraisal such as the sales price, lot size, bathroom count, bedroom count, age, location, size of the basement, condition, quality of construction, view, and GLA (gross living area). In 2011 Fannie Mae mandated appraisers to begin using UAD codes in their reports to describe all of these elements. You may have read a report and thought, “Why the heck is the appraiser saying the property is in ‘C4′ condition? What does that even mean?” Well, that is a Fannie Mae UAD code to describe a specific condition, and now that Fannie Maw has over 12 million appraisals in their system with these codes, it has allowed Fannie Mae to give birth to the CU review tool.

5 things to know about Fannie Mae’s Collateral Underwriter:

- Fannie loans only: CU is only used for loans geared toward Fannie Mae, and not for divorce appraisals or any other private appraisals. CU is also not used on 2-4 unit properties or “drive-by” appraisals.

- Not FHA/VA: CU is not used for FHA and VA loans (I’d be shocked if they didn’t adopt it later though).

- Commentary: The CU tool does not read any of the commentary by the appraiser, which can be key to understanding comp selection, adjustments, and the final value.

- Neighborhood boundaries: CU uses census block groups for data analysis instead of specific neighborhood boundaries that may be readily understood in the market. Pulling data from the right neighborhood can make a HUGE difference in a valuation, don’t you think?

- Adjustments & comps: Fannie Mae has heaps of data to compare to any new appraisals that come into the system. Not only do they know about sales in the neighborhood, but they also know which comps other appraisers have used, and even value adjustments given by other appraisers. CU knows if an appraiser says a comp is in good condition (C3) in one report, but then says it is in fair condition (C5) in a different report. CU will pay special attention to comp selection, adjustments, and the final reconciliation of value.

Potential Impact of Fannie Mae’s Collateral Underwriter:

- Unknown: The truth is we don’t really know how CU will impact the market. It could be a game-changer for the mortgage industry and appraisal profession, or it could feel like the same old same old.

- Slower loan process: As CU is implemented, expect a learning curve, and thereby a slower loan processing time. It’s going to take some time for lenders, appraisers, and underwriters to work out the bugs.

- More conservative appraisals: One of the unintended consequences of CU may be more conservative appraisals.

- Headaches for appraisers: The fear among appraisers is that lender clients will now come back to say, “CU has identified 20 other comps in this census block. Why did the you not use these?” Hopefully that will not happen (assuming the appraiser did a good job of course), but increased scrutiny will be bound to cause appraisers to spend more time responding to CU.

- Higher cost for consumers: If CU does end up putting more work on appraisers, it may lead to higher appraisal fees. After all, more work requires more time (which is money).

Advice to the Real Estate Community:

- Real Estate Agents: Make sure your clients know how strict the underwriting process has become for appraisals. I’m not saying you need to sit down with your clients and watch Fannie Mae’s CU tutorial (that’s probably a quick way to lose clients). All I’m saying is this is one more reason to price properties correctly since the appraisal is going to be even more scrutinized now. Also, if you accept an offer that is clearly out sync with neighborhood values, the lender is going to have a ton of data at their disposal about neighborhood values – even if the appraiser happens to “hit the number” somehow.

- Appraisers: Many appraisers are gravely concerned about CU, though many lenders have been reaching out to say, “Hey, we’ve already been scrutinizing you, so don’t worry about this.” Only time will tell how this will impact business and the industry. All we can do is choose the best available comparables and make reasonable market-supported adjustments. There will be a learning curve to know how to avoid red flags so to speak, but explaining why we made adjustments and supporting those adjustments will be a big theme this year for lender work. The bottom line is appraisers will need to add more commentary in their reports. If you are making the same adjustments in every single report regardless of the location of the property, it’s time to stop that because adjustments vary depending on the neighborhood. If you are struggling to support adjustments, it may be a good year to find a mentor as well as take some quality continuing education. If you do not know how to graph sales, make that a top goal this year. On the other hand, if you are an experienced appraiser, find ways to be a mentor to other appraisers by answering their questions – whether on forums or in person. As I said in 10 things appraisers can do to improve the appraisal industry, “Too many appraisers think they are right about everything, but at the end of the day being right doesn’t help anyone grow. Find ways to share your knowledge and build others up.” Lastly, if it ends up costing you more time to do your work, it may be time to consider raising your rates.

Reprinted with permission from Mr. ’s blog at sacramentoappraisalblog.com.