When your market area begins to slow down, how many times have you sat at your desk, twiddling your thumbs, gazing at the wall? Maybe you’ve cleaned your house one too many times. You may think the solution may be to step outside your comfort zone and take on an assignment a little farther outside your market area. However, you have never appraised there, nor studied the market. You may have driven through the community a couple of times, (enough not to get lost) but at the end of the day – it is not your area of knowledge or experience.

Next thing you know, you receive a call to complete an appraisal report in the next town over. So, what do we do?

If the potential assignment is for a private party, it is easy to let the client know that we have neither the experience or knowledge of the market, but that we can learn it and deliver a competently produced appraisal report. After all, the Uniform Standards of Professional Appraisal Practice does allow us to gain competency as long as we inform our client ahead of time, disclose it in the subsequent delivered report, and of course, deliver a competently completed report. Otherwise, how will we ever expand and grow?

If the client is fine with us taking the steps necessary to learn the market and deliver a credible and competent valuation report, then we can do it. This factor applies to property types (within the scope of the appraiser’s license), different appraisal products such as relocation or estate work, and it can apply to different methods of valuation.

On the other hand, if the assignment is for ABC lender, and they request the URAR form report, we cannot simply accept the assignment. What do Fannie Mae, Freddie Mac, and FHA have to say about gaining competency? What do our mortgage form reports say?

Certification 11 in the 1004 form says, “I have knowledge and experience in appraising this type of property in this market area.” It does not say that I have knowledge or experience in a different market area or different property type, but it is specific to the type of property in the market area.

Certification 12 goes on to state “I am aware of, and have access to, the necessary and appropriate public and private data sources, such as multiple listing services, tax assessment records, public land records and other such data sources for the area in which the property is located.” This means that we must have the specific sources available to us.

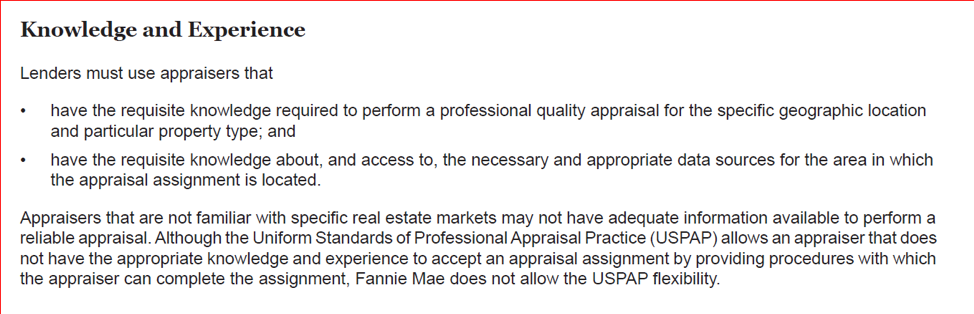

Fannie Mae requires the appraiser already have the requisite knowledge for the specific location and particular property type and access to the data sources. The Selling Guide specifically states that Fannie Mae does not allow the USPAP flexibility about gaining competency.

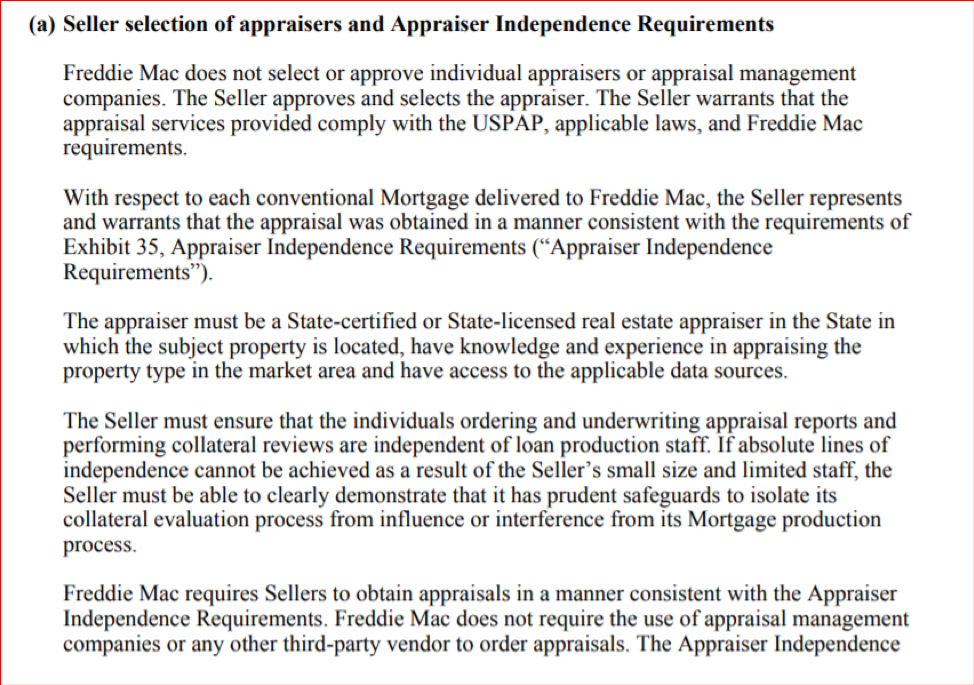

Freddie Mac has similar language, stating “The appraiser must be a State-certified or State-licensed real estate appraiser in the State in which the subject property is located, have knowledge and experience in appraising the property type in the market area, and have access to the applicable data sources.”

FHA requires the appraiser to have the knowledge about USPAP and FHA appraisal requirements, and the appraiser must meet the competency requirements prior to accepting the assignment.

The form itself, as well as the GSEs cited above, all are clear that competency has to be in place related to the area and property type prior to accepting the assignment. This means that stepping outside of our comfort zone for an area we are not yet competent in, will not work for this type of assignment.

This does not solve the problem of trying to gain experience in an area, but there are other ways to do so. Nothing precludes us from aligning with a local appraiser to gain this knowledge and experience OUTSIDE of the mortgage realm, which we can then transfer into the area later or from doing some private work and becoming competent.

If your market area is slow, you have the perfect opportunity to grow by expanding your knowledge base. Take more classes, work on solving particular problems such as finding depreciated cost from the market, studying land sales, etc. Taking the necessary baby steps to gain competency will allow us to avoid having to say “no” next time a mortgage assignment comes our way. Plus, it will save us from cleaning our house and twiddling our thumbs.

If you would like to submit an article to the Appraisal Buzz, please contact us at comments@appraisalbuzz.com.

Share this article

Written by : Rachel Massey

Rachel Massey is a designated member of the Appraisal Institute and NAIFA, a RAC member, and AQB Certified USPAP instructor. She has close to three decades in the appraisal field, working alternately between being an independent fee appraiser and on the back-end in review for several mortgage lenders. Rachel is based out of Ann Arbor where she raised and educated.

Comments are closed.